Debt challenges in MENA

A potential debt crisis might be looming in the MENA (Middle East and North Africa) region, especially for Egypt, Jordan, and Tunisia. This coupled with uncertain economic prospects worldwide is creating a perfect storm for the region. The reliance on fixed exchange rates and bad debt financing has contributed to the development of this potential crisis. Recent shocks, such as the pandemic and the spillover from Russia’s invasion of Ukraine leading to higher food prices have also contributed to soaring debt levels.

While there have always been structural issues related to governance and regulation of state-controlled economies, bloated public sectors that hinder private sector growth, and poorly targeted subsidies in these countries, the problem has been further compounded by social challenges and distrust in government. The administrations have used public debt as a temporary solution to delay dealing with economic problems-but this is without a meaningful solution in sight.

Cheap borrowing also has now become scarcer in MENA as due to lower global oil prices affluent oil producers are now reluctant to continue unconditional economic support. The problem is further exacerbated as Jordan, Tunisia, and Egypt have savings rates below 10 percent of GDP, less than a third of the global average. There is also a low level of tax revenue in these countries. Moreover, unemployment is high, primarily due to lack of good jobs.

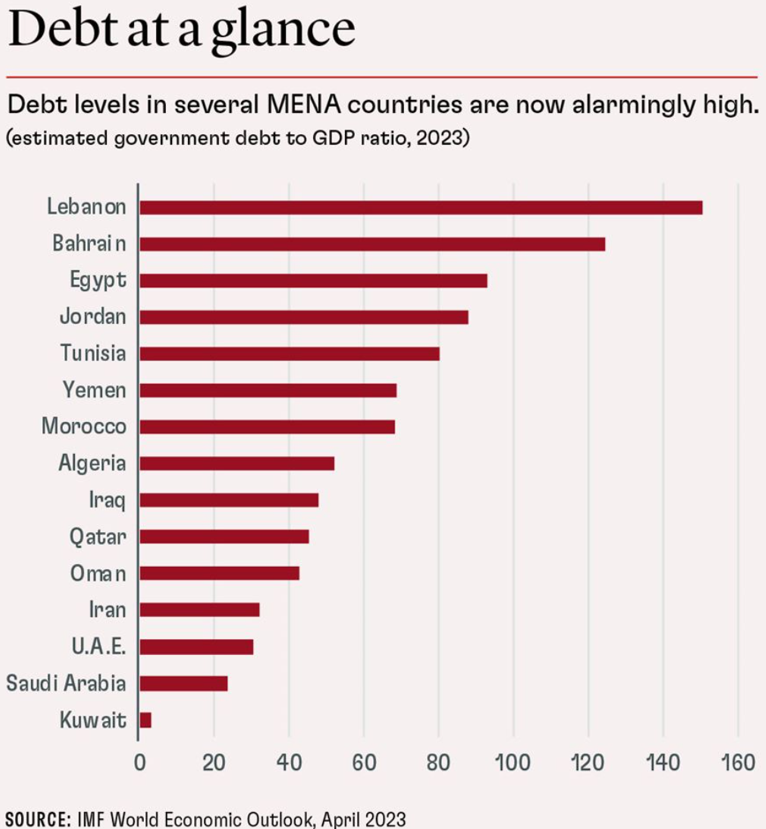

As a result of the military’s control over the economy, Egypt has endured years of economic stagnation. Aside from the pandemic’s impact on tourism, Russia’s war in Ukraine has also pushed up food import costs. With persistent budget deficits, short-term capital inflows have been necessary to meet substantial economic needs. In Egypt, gross borrowing has amounted to 35 percent of its GDP in 2023, making it highly vulnerable to economic turmoil. Jordan has also been struggling with low growth, largely due to fixed exchange rate, as well as geopolitical and economic disruptions. After the Syrian civil war, a large influx of refugees and trade disruptions have further strained its economy. Heavily relying on foreign aid, Jordan has struggled with controlling its public expenditure while being burdened with hefty subsidies and security expenditures. Among Arab Spring economies, Tunisia was the only one that appeared to take steps to advance democracy and governance. The increasing role of the government in providing employment and subsidies, as well as the COVID-19 shock that hit the economy, have put the country at economic risk. Tunisia became dependent on external borrowing, primarily from creditors who supported its democratic transition. But due to recent political upheavals, which have undermined Tunisia’s democratic progress, Tunisia is now inexorably drifting into debt distress.

Historically, we have seen the MENA region struggle with debt crises for a long time. Internal and international conflicts, as well as unfavorable global conditions, including downward swings in commodity prices, led to episodes of debt distress in the region during the 1980s and 1990s. Another series of debt rescheduling occurred in the 1990s and early 2000s as a result of regional conflicts. It was with substantial support from the international community and the international financial institutions that these debt crises were solved. However, the situation is more challenging today.

Even before the global pandemic in 2020, the debt-to-GDP ratio was rising in MENA. By 2019, 16 out of 19 MENA economies had a higher debt-to-GDP ratio than they did in 2013. The median economy’s debt-to-GDP ratio increased by more than 23 percentage points over the period, or almost 4 percentage points per year.

Now, high-debt MENA countries face the threat of unsustainable debt and a long and distressing restructuring process. Going forward, the world economy also faces a weak outlook – growth prospects are constantly being downgraded amid persistently high inflation levels. Furthermore, obtaining external financing will be a significant challenge, and if it can be obtained, the interest rates will be high. Oil-rich nations in the Gulf, which have traditionally provided substantial financing, have revised their aid strategy. Currently, they require the borrowers to demonstrate concrete and credible commitments to structural reforms, including those that will attract foreign direct investment into their economies. The recent increase in inflation will further add to the debt burden for MENA oil importers. The MENA region is forecast to grow at 2.7 percent in 2024—a return to pre-pandemic levels, although still less than the rest of the world.

Now, high-debt MENA countries face the threat of unsustainable debt and a long and distressing restructuring process. Going forward, the world economy also faces a weak outlook – growth prospects are constantly being downgraded amid persistently high inflation levels. Furthermore, obtaining external financing will be a significant challenge, and if it can be obtained, the interest rates will be high. Oil-rich nations in the Gulf, which have traditionally provided substantial financing, have revised their aid strategy. Currently, they require the borrowers to demonstrate concrete and credible commitments to structural reforms, including those that will attract foreign direct investment into their economies. The recent increase in inflation will further add to the debt burden for MENA oil importers. The MENA region is forecast to grow at 2.7 percent in 2024—a return to pre-pandemic levels, although still less than the rest of the world.

The road ahead is challenging, high-debt countries in MENA have a narrow escape route from impending debt crises, and existing policies may restrict their options. A combination of growth-boosting policies, new borrowing strategies, and a degree of fiscal consolidation may be able to mitigate these risks. In order to spur growth, Egypt should dismantle its overbearing regulatory system and diminish the role of the military in the economy. An effective privatization program that attracts foreign investment should be implemented. In order to avoid a crisis, Jordan should put deeper structural reforms in place. A number of crucial reforms must also start in Tunisia as soon as possible in order to reverse the recent erosion of democracy.