The $111 billion discount

Start with one number: $111 billion. That is how much capital flowed through Israel’s technology sector in 2025—nearly four times the previous year, comfortably surpassing the giddy peak of 2021. By any normal accounting, this should be the champagne year, even if the war mutes any celebration. Whatever the case, nobody in the real economy seems to have gotten any party invitations.

Some subtle (and not-so-subtle) shifts suggest that our growth rate has slowed relative to peer tech hubs and indications are that our gaps with global competitors have widened. High-tech’s share of GDP has been flat for two consecutive years. Startup formation is declining. The brain drain is accelerating. And the sector that was supposed to be the engine of Israeli prosperity employs about 10–12% of the workforce—leaving everyone else to contemplate apartment prices that would give a Manhattanite sticker shock.

The headline numbers tell the story. Of 260,000 people employed in Israeli tech, only 60,000 work for publicly traded firms. Half the employees of privately held Israeli tech companies are now based abroad—not just in sales, but in R&D, the function that was supposed to stay put forever. Bloomberg has reported fears of a “permanent exodus” of skilled elites, which is the kind of phrase you associate with fading states, not countries that might be prematurely running a $111 billion victory lap.

High‑tech contributed roughly NIS 317 billion to GDP last year—17.3% of the national total—virtually unchanged from 2023. The sector is getting richer even as its growth rate flatlines. Meanwhile, Israel’s GDP per hour worked runs 20–25% below the OECD average and 40% below the top performers. Israelis work longer hours than nearly all their peers yet produce less for each one—the economic equivalent of flooring the gas while stuck in neutral.

The reason is structural: Israel doesn’t have one economy; it has two. High‑tech workers generate about 160,000 dollars per worker in purchasing‑power terms, compared with 83,000 dollars in the domestic sectors that employ the vast majority. Milken Fellow Gilad Brand (now Lead Applied Research Economist at the Finance Ministry) has mapped what is essentially a dual economy under a single flag: a small, globally competitive tech enclave—a kind of gated penthouse economy—built on crumbling stairs of trade, construction, local services, and low‑tech manufacturing where productivity growth has stalled. The wall around this penthouse is remarkably solid—limited labor mobility, yawning skill gaps, under‑investment in infrastructure, and sheltered domestic markets that feel little competitive pressure to modernize. Innovation stays upstairs. Everyone else gets Silicon Valley prices on decidedly non‑Silicon Valley paychecks—as the cost of living keeps climbing.

There is, however, genuinely good news. When the Milken Innovation Center convened its first Financial Innovations Lab on Israel’s capital markets in 2014, the Tel Aviv Stock Exchange was quietly expiring. Daily trading volume had cratered by half, liquidity ranked 31st globally, and 95% of startups were being sold to foreign buyers rather than going public at home. The diagnosis was blunt: Israel was building world-class companies but lacked the financial plumbing to keep the value they created.

Of fifteen reforms proposed at that Lab, at least ten have been substantially enacted. TASE demutualized and listed itself in 2019. The exchange shifted to Monday–Friday trading in January 2026. Market-making reform reduced spreads by over 80%. A Technology 35 index launched. And TASE UP created a platform for private companies to tap institutional capital without a full public listing. The TA-125 surged 51% in 2025, outperforming the S&P 500 and Nasdaq. Foreign investors poured over $2.3 billion into TASE equities. Daily trading volume reached NIS 3.8 billion—nearly five times the nadir that prompted the original Lab.

All of which is impressive. And all of which has still not been enough.

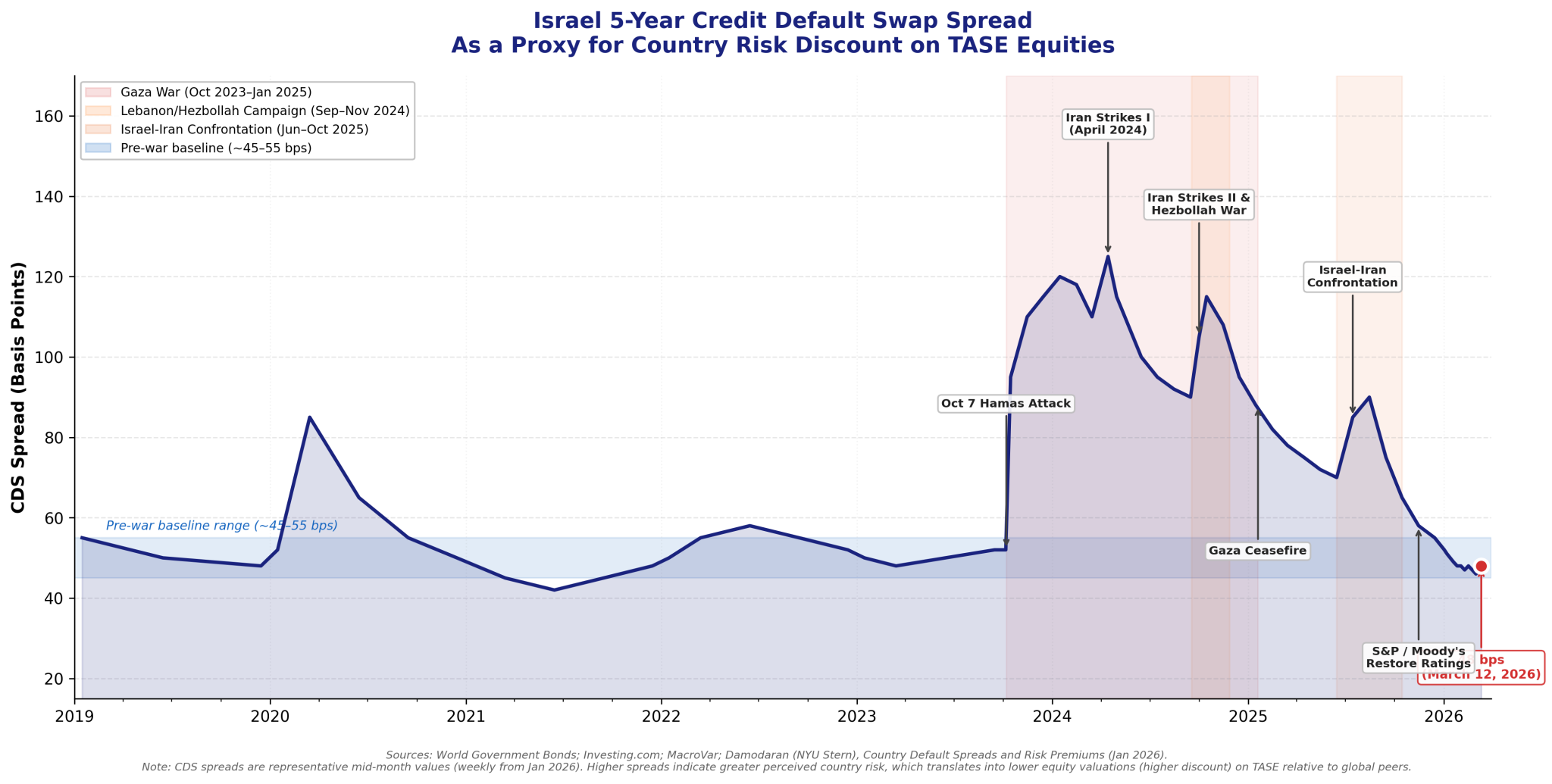

One reason is visible in a single comparison. The Israeli market currently trades at a price-to-earnings ratio of roughly 20x, versus about 24x for the MSCI World index—a valuation discount of approximately 17%. That gap is the country-risk discount, and it is not merely an abstraction for portfolio managers. It means that Israeli companies raising capital on TASE are valued at less than comparable firms elsewhere simply because they are domiciled in Israel. For a founder deciding where to list, the arithmetic is brutal: the same earnings stream is worth roughly a fifth less in Tel Aviv than in New York.

Put another way: with the TASE’s total market capitalization now around 600 billion dollars—boosted in part by a stronger shekel rather than a sudden leap in underlying earnings—a 20% discount translates into roughly 110–112 billion dollars of “missing” value, companies priced below what they would command on a comparable exchange without Israel’s country‑risk premium. That is the bill Israel pays for capital markets that do not yet match the scale of its innovation. And this is not a wartime distortion; it is the peacetime baseline. During the post‑October 7 peak, when sovereign CDS spreads roughly doubled, the implied discount was far steeper—potentially 150–200 billion dollars in foregone market capitalization. Closing even a quarter of that structural gap would unlock 25–30 billion dollars in additional value: deeper liquidity, higher valuations, more listings, and less pressure on founders to sell early.

Here is the feedback loop the paradox ultimately rests on: the country-risk discount makes it harder for Israeli companies to raise capital domestically at competitive valuations, which pushes them offshore, which prevents the deepening of domestic markets that would eventually compress the discount. Breaking that cycle requires exactly the kind of capital-markets infrastructure buildout the Lab is designed to address.

Israeli pension funds—managing over NIS 2.5 trillion—have actually been reducing their high-tech and VC exposure. Institutional investment directed to Israeli investment funds has fallen from 40% a decade ago to under 20% today. Israel still lacks a Business Development Corporation framework or other public-private capital bridge building, a functioning securitization market, or the late-stage financing infrastructure that would keep scaling companies at home rather than pushing them offshore.

This is where the human story meets the structural one. Israeli entrepreneurs don’t sell out too early because they lack ambition. They sell early because the financial infrastructure gives them no viable alternative. A typical startup raises seed and Series A domestically, builds a product, finds traction—and then hits the growth stage, where it needs $50–150 million to scale, and discovers that the money simply isn’t there at home. Pension funds are pulling back. There’s no deep secondary market where early investors can get liquidity without forcing a full exit. So the founder faces a choice that isn’t really a choice: redomicile, list abroad, where the upside accrues to foreign investors and foreign tax jurisdictions; or accept an acquisition from a multinational that wants the technology and the team, take a respectable but premature return, and watch the real value creation happen inside someone else’s balance sheet.

Most take one of those two doors, because the third option—scale at home, go public on TASE, build a large independent Israeli company—requires late‑stage infrastructure that still doesn’t really exist. The financing gap acts less like a barrier and more like a trap door: companies fall through it not at the point of failure, but at the point of success. A 500 million‑dollar acquisition may look like a win, but if that company had been worth 5 billion dollars as an independent public company five years later, that is 4.5 billion dollars in value—along with the jobs, the IP, and the tax revenue—that has been exported. For a sector the government has spent decades incubating, that is a lot of public investment left on the table—and it is the arithmetic the 111‑billion‑dollar headline conveniently leaves out.

Policy innovators have not been idle. Yozma 2.0—$1 billion in government-matched VC investment—was oversubscribed. The first Israeli sovereign green bond was six times oversubscribed. The November 2025 VC tax reform reduced carried interest taxation and created favorable treatment for foreign LPs. These are serious moves.

But the cautionary tales matter too. The 2017–2018 high-tech mutual fund tender achieved barely a quarter of its NIS 1.6 billion target. The R&D limited partnerships enabled in 2019 produced near-total losses—Millennium Food-Tech trades at a 98.5% decline from its IPO price, the kind of number you read twice to check the decimal. These initiatives failed because they grafted venture capital strategies onto regulatory structures designed for something else, without the frameworks that make similar vehicles work abroad: pass-through tax treatment, closed-ended funds, secondary-market liquidity. They asked investors to take venture-level risk with mutual-fund-level governance. Investors noticed.

Israel’s tech economy is not merely a collection of startups with clever founders and good hummus in the break room. It is a complex ecosystem requiring capital markets infrastructure at every stage—from formation through late-stage growth to public listing. When that infrastructure has gaps, capital and companies flow elsewhere. This is not disloyalty. It is financial physics. The reforms still needed are neither mysterious nor unprecedented: exchange-listed growth finance frameworks adapted to Israeli conditions; a technology bridge to institutional investors for pre-IPO trading; reformed R&D vehicles with adequate scale; and regulatory changes giving pension funds the permission and incentive to allocate meaningfully to domestic high-tech in AI everywhere, deep tech, food, health, energy, and and climate-tech. The securitization legislation, the repo market, and the NYSE–TASE partnership ideas point the right way. In January, a visit to Jerusalem by the U.S. SEC chair, focused on exploring mutual recognition of securities regulation, signaled ongoing work to ease cross‑listing and capital‑raising between Tel Aviv and New York. These initiatives need company.

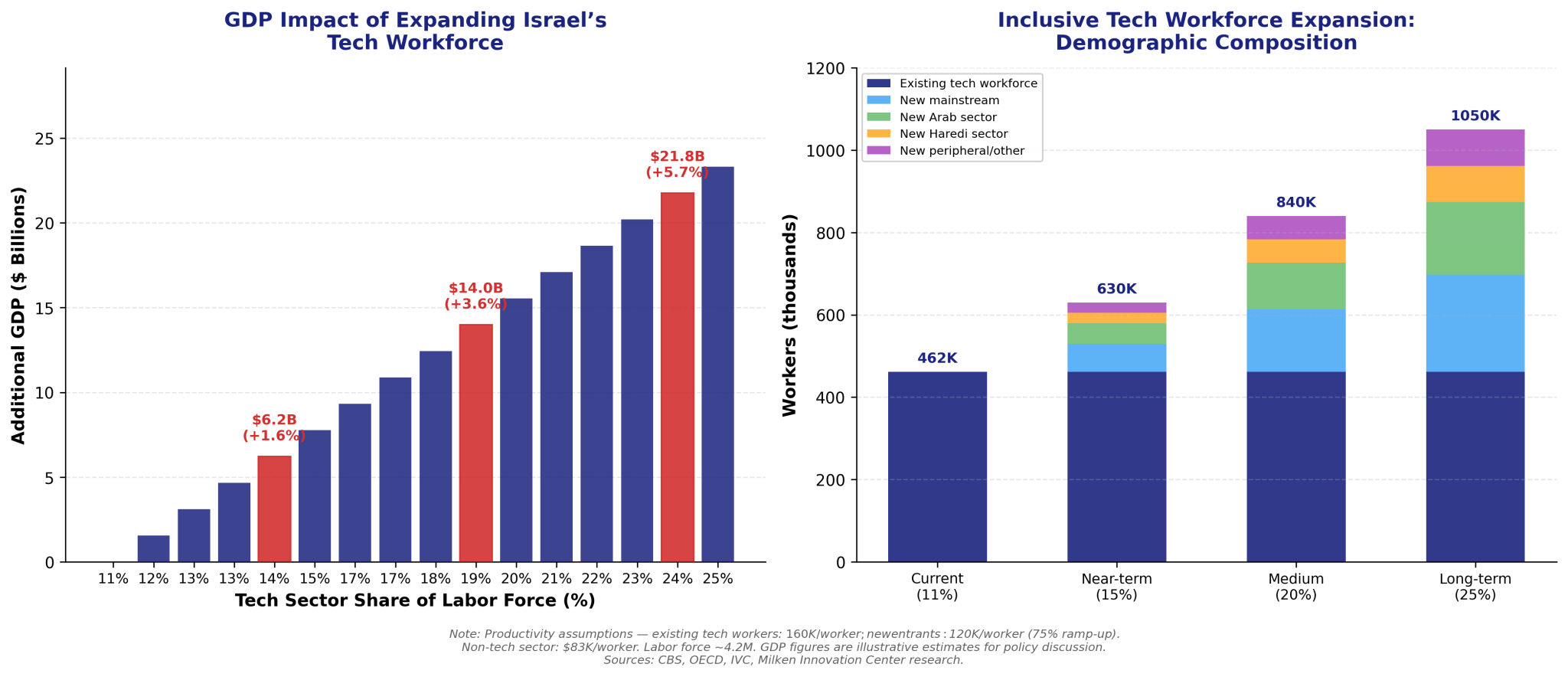

There is, however, a way to address Israel’s productivity gap and its inequality problem in a single move. Today, roughly 11% of the labor force works in the high-value tech sector—generating $160,000 per worker against $83,000 in the traditional economy. The remaining 89% are effectively locked out. Arab citizens, who constitute 21% of the population, hold barely 3% of tech jobs. Ultra-Orthodox communities—the fastest-growing demographic—are almost entirely absent. Peripheral populations in the Negev and Galilee participate at a fraction of the rate of Tel Aviv.

If capital-markets reform kept more tech companies scaling at home rather than exiting early, the domestic employment effects would be substantial. Our modeling suggests that expanding the tech workforce from 11% to 20% of the labor force—roughly 380,000 additional workers—would add approximately $14 billion to GDP, a 3.6% boost. Reaching 25%—an additional 588,000 workers, deliberately drawn from Arab, Haredi, and peripheral communities alongside mainstream expansion—would generate roughly $22 billion in additional output, a 5.7% gain. Even these estimates are conservative: they assume new entrants reach only 75% of existing tech-worker productivity and exclude the multiplier effects of human capital investment (health and education), higher domestic spending, retained tax revenues, and reduced social transfers.

Figure 2. GDP impact of inclusive tech workforce expansion and demographic composition of new entrants. Sources: CBS, OECD, IVC, Milken Innovation Center research.

Figure 2. GDP impact of inclusive tech workforce expansion and demographic composition of new entrants. Sources: CBS, OECD, IVC, Milken Innovation Center research.

The point is not merely economic. An Israeli tech sector that includes Arab engineers from Nazareth, Haredi data scientists from Bnei Brak, and biotech researchers from Beer Sheva is not just a more productive economy—it is a more cohesive society. The same capital‑markets infrastructure that would narrow the TASE discount and keep companies at home would also create the employment pipeline that absorbs workers from precisely the communities currently locked out of the high‑value economy, dialing down some of the very grievances that fuel today’s toxic polarization. In that sense, solving the productivity problem and the inequality problem are not competing priorities; they are the same priority, viewed from different ends of the same capital‑markets gap.

If the tech sector continues to concentrate in a handful of mega‑firms while the broader ecosystem erodes, the consequences will reach far beyond the trading floor. An economy in which barely one in ten workers participates in the high‑value sector while everyone else struggles with unaffordability is neither sustainable nor stable—and it weakens the social cohesion that underpins Israeli resilience in the face of food, health, water, energy, and security shocks.

Israel has already shown that determined reform can transform capital markets; the TASE of 2026 is unrecognizable compared with 2013. But the paradox at the heart of the 111‑billion‑dollar year tells us the agenda is unfinished. That is what we propose to take up in our next Financial Innovations Lab: not to rest on the progress already made—though it deserves celebrating—but to design the missing financial instruments and institutions that can close the capital‑markets gap. They will determine whether Israel’s innovation capacity finally delivers broad prosperity at home, or continues to be realized on balance sheets somewhere else entirely.

____________________________________

This article is based on a recently published policy brief, “(Re)Inventing Israel’s Capital Markets: A Decade of Impact and an Unfinished Agenda” available at: www.milkeninnovationcenter.org