It’s Just Nuts

When I transferred to MTA in my sophomore year in high school and began living in its dormitory, one of the first things my roommates and I did was sign up for a

subscription to the New York Times. The price was so low it almost felt like they were paying us. They probably figured that was the best way to hook lifetime readers and subscribers; it certainly worked with me ¬– a daily subscriber and reader from that day to the present.

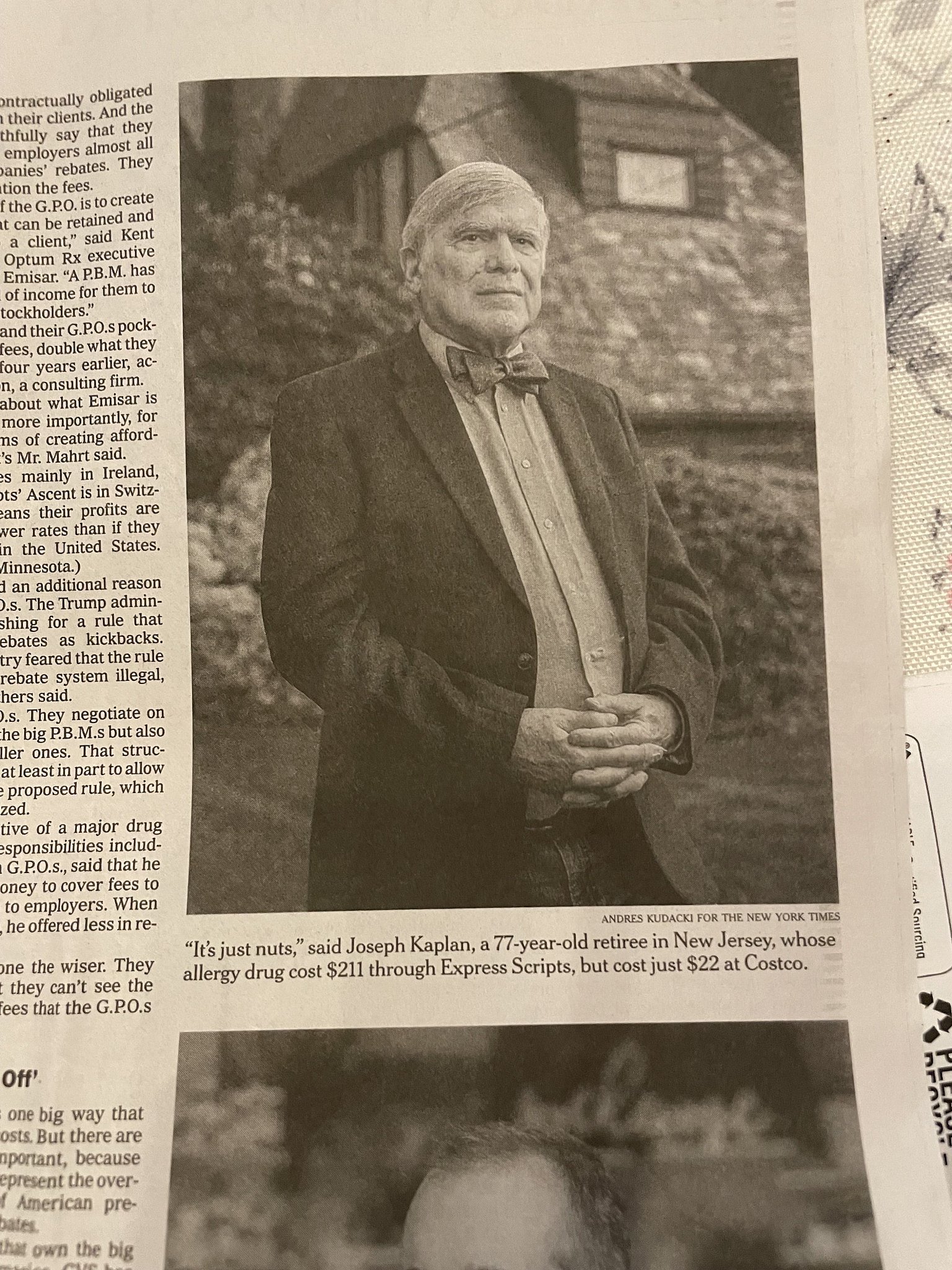

My other strong connection to the Times is their letters-to-the-editor section where 19 of my letters have appeared. (I won’t tell you how many I’ve sent since the low percentage diminishes the effect of the absolute number.) But until this past week I’ve never been interviewed by the Times nor had my picture appear in the news columns. Well, as you can see from the attached picture, a recent article eliminated one more item from my bucket list.

That front-page article, “A Shadow Industry,” is an expose of pharmacy benefit managers (PBMs) like CVS’s Caremark, Cigna’s Express Scripts, and United Health Care’s Optum Rx, which negotiate drug prices and decide which drugs are covered by insurers. The article shows that PBMs, together with insurers, drug manufacturers, and others, act in concert to drive up drug costs for millions of people, employers, and the government, including programs like Medicare. Since I had some personal experience with inflated drug prices, I was one of more than 300 people interviewed. My hour-long interview was condensed into one short paragraph that included just one of several examples of overcharges I personally experienced, and one short, but punchy, quote that sums up the drug industry’s insurance pricing: “It’s just nuts.”

One of my take aways of this story is that PBMs, manufacturers, insurers, and others intentionally make drug pricing in the United States so opaque with numerous middlemen, fees, discounts, rebates, and more, that it is impossible to truly understand why medications cost what they do and why different sources charge vastly different amounts for the same medications. Indeed, what particularly struck me was that although the article contained numerous specific instances of clear-cut overcharging, and numerous drug and insurance executives were asked for comments, none addressed or explained a single instance of overcharging. Rather, the canned answer, repeated in various locutions, was: while we can’t address that specific case, we save consumers billions of dollars a year overall. Hah!

But the purpose of this column is not to repeat the findings of the Times article. Rather, it’s to do three things: give a short primer on Medicare, tell two specific drug overpricing tales that didn’t make the article, and discuss some methods to better navigate Medicare both overall and especially with respect to prescription drugs. While I don’t have any answers or solutions to this national problem, perhaps I can actually save you some money.

Medicare

1. Those eligible for Medicare can enroll in one of two different types: original Medicare or Medicare Advantage. Original Medicare, consisting of Parts A (hospital services), B (doctor services and procedures), and D (prescription drugs), is a federal program whose first two parts (A and B) are run by the Department of Health and Human Service’s Centers for Medicare and Medicaid Services (CMS). The third part (D) is purchased from and managed by insurance companies.

Medicare Advantage (Part C) is also purchased from and managed by insurance companies. It’s all-inclusive and takes the place of Parts A, B, and D. Its advantages include a cheaper premium, additional coverage for services like vision, hearing, and gym memberships, and a yearly cap on out-of-pocket costs. Its disadvantages include the requirement to use the insurers’ often limited health care provider networks, the necessity of obtaining referrals to see a specialist, and having for-profit insurance companies approving and denying claims. (More on this later.)

2. Original Medicare has an established price for each covered service, and pays the provider 80% of that amount; i.e., if a doctor charges $500 for a service but Medicare’s approved charge is $300, CMS pays the doctor $240 for that service (80% of $300). The remaining 20% of the approved charge (i.e., $60) is the patient’s responsibility. Patients are not responsible, however, for the $200 difference between the Medicare rate and the provider’s charge; providers call that an “insurance discount” and write it off.

Medicare beneficiaries often buy insurance – called Medigap or supplemental insurance ¬– to cover the 20% of the Medicare approved amount they are responsible for (less a copay, for some services, of no more than $20), which drastically limits their out-of-pocket costs. Medigap, like Part C and D, is purchased from insurance companies and not CMS, though the terms of coverage are strictly delineated by government regulation, including the requirement that Medigap cover all Medicare approved services provided by every Medicare provider, with no discretion to deny a CMS-approved claim.

3. Part D prescription drug insurance policies managed by for-profit insurers are very complex. For purposes of this column, however, I’ll limit myself to just a few critical elements. First, in each state there are a number of insurance companies that offer such policies. Companies charge different premiums and have different formularies (a listing of the medications they cover), deductibles, and costs for the medications. Patients can change policies every year if they choose to and many do.

If a medication is included in the formulary, the patient can buy it from any pharmacy with the patient and insurance company sharing the cost in a way that is often difficult, if not impossible, to understand, as the examples in the next section show. However, each company has preferred pharmacies which are supposed to offer consumers better prices for the medications, with the cheapest way to order medication, the insurers suggest, being a 3-month supply from the insurer’s preferred mail order pharmacy.

Sharon and I are enrolled in original Medicare and this year use WellCare as our Part D insurer. WellCare’s preferred mail order pharmacy is Express Scripts (which is also a PBM).

Inexplicable Prescription Drug Prices

I recommend the Times article for a detailed discussion of the process of how prices are negotiated and determined, though, as I noted above, the process, even after all the Times’ investigation and analysis, remains opaque. One thing is clear, however; prices are often inflated. I won’t rehash the information in the article. Rather, I’d like to describe two specific price overcharge cases I have personal knowledge of which will help explain some of my suggestions for navigating the system.

When we first tried to renew one of our medications this year, we were told by Express Scripts (WellCare’s preferred mail order pharmacy) it would cost $186.07 for a 90-day supply. Since I knew that price was much higher than we paid last year, I asked my local Costco pharmacy for a quote even though Costco is not a preferred WellCare pharmacy. I gave Costco our WellCare insurance information and was told that its price was $56.76, a discount of 70% off Express Scripts’ charge. I’m sure you’ve figured out where we ordered from.

But when it was time to renew I tried, based on a recommendation, a different approach. I asked the Costco pharmacist what the medication would cost if they didn’t put it through our WellCare insurance. The answer: $18, which is what we paid the second time.

The math is simple. WellCare and Express Scripts, its PBM and supposed preferred pharmacy, wanted to charge us TEN TIMES what Costco actually charged without WellCare’s participation. As I told the Times: It’s just nuts.

A second example raises even more questions. I use an inhaler for which Costco charges, without insurance, $250 per inhaler. So when I ordered one from Express Scripts for $190 earlier this year, I thought I was saving $60 per inhaler. At refill time I decided to check with Costco again, and was told that if Costco put the order through my WellCare insurance, three inhalers would cost $274.16 – almost $300 less than what Express Scripts would have charged for three ($190×3=$570).

The opaqueness as to price only increased when I received my Explanation of Benefits (EOB) form from WellCare. The “drug price” listed on the EOB for the three inhalers I bought at Costco was $487.87, of which I paid $274.16 and WellCare paid $213.71. I understand the math – I was always good at addition and subtraction. But what I don’t understand is why Express Scrips had charged me the equivalent of $570 for a medication that had a “drug price” of $487.

Where does the $487 come from? How does it relate to any of the prices I received from Costco or Express Scripts with or without insurance? Opaqueness buried within opaqueness, with nothing making any sense. Rather, the purpose of the entire process seems to be to make it impossible for consumers to understand pricing so they’ll give up and pay whatever the insurers and PBMs demand. To quote myself again, it’s just nuts.

Suggestions

I don’t want to leave you only with questions, so let me pass on some strategies to get the best overall Medicare coverage and also, hopefully, save some money.

Original Medicare vs. Medicare Advantage. As I’ve noted, choosing original Medicare rather than Medicare Advantage means paying more to obtain certain benefits. I’ve personally found those benefits worth that additional cost. Your situation, of course, might be different. I’d note, though, that since enrolling in Medicare 11 years ago, my wife and I, who have used numerous health care providers over that time, have never come across one who was not a Medicare provider – not surprising since 98% of doctors are Medicare providers. Those enrolled in Medicare Advantage, however, are limited to being treated by the insurer’s much smaller network. Moreover, Medicare has never denied or delayed paying a single claim as, I’ve read, many Advantage insurers do. Plus, we’ve found that not having to get referrals for specialists is a major convenience and time saver. My suggestion: seriously consider original Medicare.

Medigap/Supplemental Insurance. Medigap insurance, unlike traditional health insurance, performs only ministerial chores like writing checks to health care providers and sending EOBs to Medicare beneficiaries. It does not require you to use the insurer’s health provider network, nor does it have the ability to deny or delay approving or paying claims.

This means that the only relevant difference between Medigap policies is the amount of their premium. And, as I learned relatively recently, there’s a range of premiums among different Medigap insurers. So with the help of an independent insurance broker, we found a new Medigap insurer whose premiums for me and my wife are about $1200 a year less than our previous policy. And since the broker is paid by the insurer and not the insured, there was no cost to us in finding the policy and switching to it. Thus, everyone with a Medigap policy should shop around and buy a policy based solely on premium price.

Part D prescription drug coverage. My suggestion here takes more work. Before this year, I thought shopping around for prescription drugs was unnecessary; just order a 3-month supply of the medication from the insurer’s preferred mail order pharmacy and I’d get the lowest price. But I learned my lesson. Thus, for every expensive medication (less expensive ones called tier 1 and tier 2 drugs are very cheap wherever you get them), I suggest you do what I do now. First, ask your doctor to call in the prescription to your mail order pharmacy with directions not to put the order through until you approve it. Also, get a paper script from the provider. Then take the script to a local pharmacy like Costco and ask what their price is for the medication both with and without insurance. Compare all three prices and order the least expensive. It’s not easy and it is time consuming. But as you can see from my examples, it can save significant dollars.

Conclusion

One last question. Why write about this in the Jewish Standard. One snippy answer is that the Times gave me only one short paragraph; the Standard is giving me over 2,000 words. More seriously, though, I would have been very thankful, and my bank account more robust, had someone imparted this information and these suggestions to me several years ago. I’m therefore unhappy that the for-profit insurers, PBMs, and their allies withhold this information from consumers in order to increase their profits. Thus, following Hillel’s famous aphorism – that which is hateful to you do not do to another (Shabbat, 31a) – I decided not to withhold from others what I have learned. This column is therefore my personal small contribution to dealing with America’s unintelligible health insurance system.