Why Tel Aviv Property Prices Aren’t and Still Won’t Go Down

Ten years ago, I wrote an article on these very pages titled “Tel Aviv is Different: Why Property Prices Aren’t, and Will Not Go, Down…” Looking back, I can’t help but think to myself what a prophetic assertion that was. In 2012, global markets were reeling from the still fresh real estate meltdown and Israel real estate was experiencing turmoil. Most of my clients who did not buy then bitterly regret it today. Today, the market is experiencing similar if not identical jitters and the number of transactions has come to a simmer.

The factors are somewhat different than the Lehman Brothers aftermath, but the reaction is a serious “déjà vu”. The past is no indication of the future, that’s what people tell me , and the situation back then was not as serious as it is today, others retort. I, however, beg to differ. Allow me to answer these claims and add an extra element that make the Tel Aviv real estate market continue to be an attractive investment sector that will stand the test of the current global economic climate.

The market dislocation of 2009 was indeed real estate induced. Arguably the MBS (mortgage backed securities) market meltdown that started at Bear Stearns in 2007 and flowed globally did not directly affect the Tel Aviv real estate market but definitely put a damper on the foreign investment. The interesting point is that the local MBS market is as developed as it was when I wrote that article. That is to say that it is practically nonexistent. Secondly, the current crisis has nothing to do with real estate. It’s a combination of exogenous factors where inflation holds center stage. Inflation has been headlining the financial and economic news for the last year.

Not all inflations are borne the same however. The combination of the loosening monetary policies, the government Stay-at-Home compensation programmes and the COVID related logistical bottlenecks have all contributed to the acceleration of the price increases. Those causes however are being tackled through a normalization of the supply chain and the aggressive interest hikes across the globe. Since the beginning of the year, stock markets which some see as a crystal ball have had an extraordinary bull run, indicating that the increased confidence of the main institutional and private investors that the worst has passed.

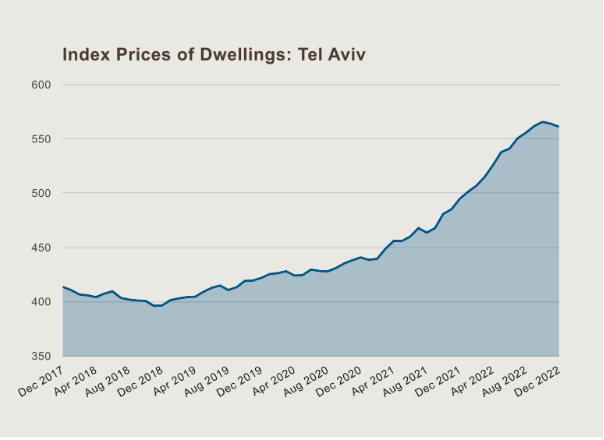

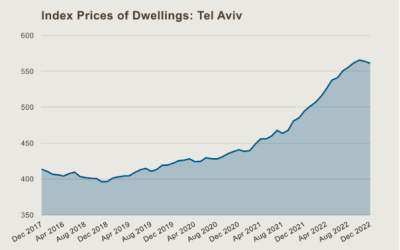

The real estate market is lagging the stock market, that’s a universal truth that even skeptics have to concur with. Interest rates have gone up in Israel too, yet there are not instances of fire sales and or major developers’ bankruptcies, with mortgage arrears and defaults actually lower today than in 2020. The promised “scorched earth” of the market has not materialized. So as in the immediate post Lehman era, the market has frozen and the number of transactions crashed. Have prices?

The short answer is no, and I’ll quote myself here: ”Anyone that tells you that prices are down 10-15% is gravely mistaken.”

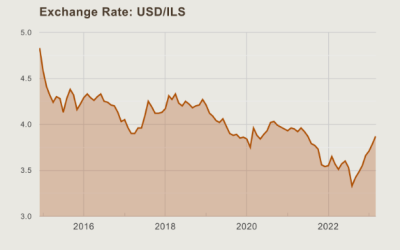

Has negotiation power shifted? The answer to that question is unequivocally, YES. As markets are dictated by psychology first and foremost, for the first time in 15 years we are seeing sellers and developers more flexible and more down to earth in terms of pricing. In addition to this, the Israeli currency, the Shekel, has dramatically decreased in value relative to the Euro and Dollar. Some will say it is due to the flight of capital in the wake of the political crisis surrounding the proposed judicial reforms of the Israeli government, but this story has been playing out for much longer.

Some will say it is due to a loss of confidence in the state of Israel government, and some others will say, this is a Dollar story, not a Shekel story. No matter what the reasons for this currency correction, we think it is long-overdue and is definitely timely. You should know also that the Bank of Israel tactically slowed its interest hikes before the Fed started winding down its tightening cycle.

That widening interest differential in and of itself is enough to explain much of the shekel slide. My point here is that whether you think the Shekel slipped over 15% against major currencies is political, monetary or fiscal, you’ll agree that these are transient factors and do not reflect a fundamental real economic shift in trends. The shekel will go back up.

The question is when. I do not have the answer to that, unfortunately. What I do know is that in my nearly two decades as an advisor and broker in this market, I have never seen both a softening of the prices AND a softening of the currency occurring at the same time.

If you ask me, I think this is a perfect alignment of the stars. If you are in the market for an apartment, your dollars can get you a lot more than they could, even 12 months ago. And to answer those that understandably have concerns about the political climate, you should know that political crises, wars, missiles and threats have had, in the recent past, zero impact on the prices of apartments. The ultimate decision maker in Tel Aviv property prices was and still is the fact that there is little residential development, low LTV mortgages, a rising net-disposable income, low mortgage arrears, and a real demand that simply is not being met in any segment of the market.

All statistics are sourced from the Israeli Central Bureau of Statistics and the graphs are the copyright of the Tel Avivi Real Estate Advisory. All exchange rates are sourced from Google Finance.